Jul 28, 2025

Why Africa Needs Open Banking Regulation Now

Introduction

More than 370 million African adults remain unbanked—yet mobile money penetration is among the highest globally. Open Banking is the missing bridge: a catalyst for inclusive economic growth and innovation across the continent.

Unlike mature markets where Open Banking is evolving gradually, Africa has a unique opportunity to leapfrog legacy systems and build unified, interoperable financial infrastructure from the ground up. This can unlock new markets, reduce costs, and empower millions with seamless access to credit, payments, and digital financial tools. With robust mobile money networks already in place, Africa is uniquely positioned to rapidly scale Open Banking innovations and further amplify financial inclusion.

But realizing this vision requires bold regulatory leadership. Without clear, harmonized frameworks for data sharing, API standards, and consumer protection, Africa risks fragmented systems that stifle innovation and widen financial inequality.

This article explores why now is a critical moment for African regulators and financial institutions to collaborate and act decisively—transforming Open Banking from buzzword into a sustainable engine of growth, inclusion, and digital resilience.

What is Open Banking and Why Does It Matter?

Open Banking enables secure, consent-based sharing of financial data between banks and third-party providers (TPPs) through standardized APIs. At its core, it's about opening up financial infrastructure to unlock competition, drive innovation, and give individuals and businesses greater control over their financial lives.

Initially launched as a regulatory initiative in the UK and Europe (via PSD2), Open Banking has since become a global movement. Countries across Asia, Latin America, and Australia are implementing tailored frameworks.

The results are tangible. In the UK alone, over 7 million consumers use Open Banking-enabled services. The ecosystem processes more than 7 billion API calls and 22 million payments monthly, contributing an estimated £4 billion in economic value.

In Africa, fintech innovation is booming. According to Partech's 2024 report, fintech startups raised over $1.4 billion, representing 60% of all tech equity funding on the continent. Yet integration remains a costly barrier: in fragmented markets, fintechs can spend up to 40% of their technical integration budgets on building and maintaining custom APIs. Without standardized regulation, much of this effort is duplicated—slowing time to market and limiting scale.

For African markets, Open Banking represents more than convenience. It's a catalyst for financial inclusion, access to credit, and a new wave of homegrown fintech innovation. It also offers compelling regional value: in economic unions like UEMOA and CEMAC, harmonized Open Banking standards can dramatically lower integration costs, support cross-border innovation, and expand access to a shared digital market. A single set of standards operating across multiple countries helps scale solutions faster—fueling trade, investment, and economic growth across the region.

Regulatory vs. Market-Led Open Banking: Why Regulation Is Key

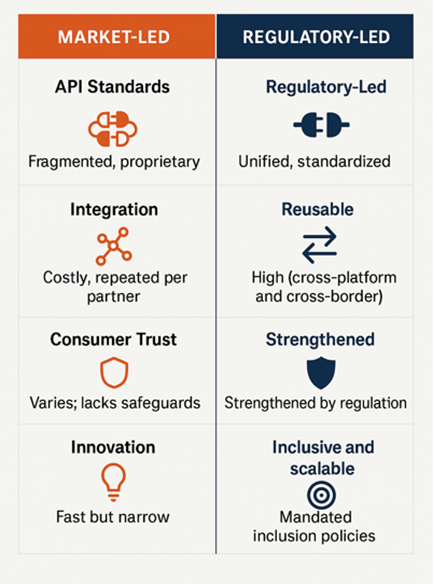

Africa's financial innovation has been impressive, but relying on market-led initiatives alone risks entrenching fragmentation and inefficiency. While fintech-bank and telecom-bank partnerships have driven rapid adoption of digital payments and mobile wallets, these efforts often remain siloed—with limited interoperability and inconsistent data governance. Fintechs operating across borders often face high integration costs due to inconsistent APIs—slowing time-to-market and stifling broader innovation.

A unified, regulatory-led approach is essential to unlocking the full potential of Open Banking. Comprehensive frameworks—like Nigeria's Open Banking regulation, which mandates standardized APIs, clear data categories, and licensing tiers—provide the guardrails and confidence needed for responsible, scalable growth. These frameworks reduce duplication, lower integration costs, and create a level playing field for both incumbents and challengers.

Figure 1: Comparing Open Banking Outcomes: Market-Led vs. Regulatory-Led Approaches

Figure 1: Comparing Open Banking Outcomes: Market-Led vs. Regulatory-Led Approaches

Regional efforts, such as UEMOA and CEMAC's central bank-driven payment systems, have processed billions in transactions and demonstrated the value of harmonized infrastructure. However, these initiatives remain largely limited to payments, without addressing the broader API and data-sharing frameworks that define true Open Banking. What's still missing is a long-term regulatory vision covering data rights, user consent, ecosystem governance, and shared API infrastructure.

In Morocco, the Open Banking journey is currently market-led, supported by strong growth in digital payments and wallet adoption. The national switch SWAM processed 401 million card transactions and 5.3 million mobile-wallet payments in 2024. Active mobile wallets now exceed 10 million, and digital payments continue to rise. In 2025, Morocco joined the Pan-African Payment and Settlement System (PAPSS), enabling real-time cross-border payments across Africa. These infrastructure gains reflect both fintech momentum and institutional support. Bank Al-Maghrib is actively exploring a formal Open Banking framework to build on this progress.

Central banks are uniquely positioned to lead this shift. By setting open standards, enabling cross-border interoperability, and safeguarding financial stability, they can catalyze a new era of inclusive, innovation-driven finance across Africa.

To make this vision a reality, collaboration is key.

The Role of Strategic Partnerships and Collaboration

No single player can build the future of Open Banking alone. Strategic public-private collaboration is not just beneficial—it's mission-critical. Public-private partnerships (PPPs) and fintech-bank alliances are the engines that turn regulatory frameworks into real-world impact.

Financial institutions provide trust, compliance, and distribution scale. Fintechs inject agility, new technology, and user-centric design. Effective collaboration can take many forms:

-

Co-developing products for underserved segments,

-

Modernizing legacy systems through API integration,

-

Launching innovation sandboxes to safely test new ideas,

-

Building cross-border payment solutions that strengthen regional trade.

Success stories across Africa highlight the transformative potential of coordinated efforts. M**-Pesa** in Kenya and EcoCash in Zimbabwe—owe their scale and impact to strong public-private partnerships. These platforms show how coordinated efforts between regulators, telecoms, and banks can deliver inclusive, mobile-first services at scale. Similarly, South Africa's Project Khokha—a regulator-led blockchain pilot—demonstrated the viability of secure, high-throughput settlement infrastructure using emerging technologies.

Looking ahead, governments, central banks, and development finance institutions must actively facilitate these partnerships. This includes investing in shared infrastructure, mobilizing catalytic funding, supporting regulatory sandboxes, and co-governing data frameworks that reflect the voices of all key stakeholders. Only through such aligned, cross-sector collaboration can Africa build a truly open, standardized, and inclusive digital finance landscape.

In developing countries, governments also have a critical role to play by investing in public digital infrastructure (DPI). By building secure, shared enablers—such as digital identity systems, e-KYC, API gateways, Instant Payments, and consent management frameworks—they can reduce barriers to entry and create the foundation for safe, scalable innovation.

Successfully Implementing Open Banking

Successful implementation requires planning, regulatory clarity, and inclusive execution. Key priorities include:

✅ Developing Comprehensive API Standards: Define interoperable, consistent API specifications to ease integration, reduce costs, and ensure a coherent user experience across the financial ecosystem.

✅ Establishing Strong Cybersecurity Measures: Secure consumer trust through end-to-end protections. Conduct regular audits, monitor threats proactively, and respond rapidly to vulnerabilities.

✅ Performance Monitoring and Incentives: Define measurable KPIs and introduce incentive systems that reward progress and penalize delays or non-compliance. This encourages continuous improvement and alignment with ecosystem goals.

✅ Promoting Financial Inclusion: Leverage mobile wallets, instant payments, and agent networks to serve underbanked and underserved populations. Design inclusive services that reflect local realities and usage patterns.

✅ Transparent and Inclusive Stakeholder Engagement: Involve regulators, banks, fintechs, and consumer advocates from day one. Co-creating solutions ensures buy-in, shared ownership, and smoother implementation.

✅ Robust Operational Frameworks: Clarify roles, responsibilities, and dispute resolution mechanisms. Transparent liability models and consumer protections must be built into the core framework.

In five years, success would mean: secure, interoperable APIs across major markets, thriving fintech ecosystems supported by clear regulation, and millions of Africans using digital financial services built on a unified Open Banking backbone.

Pitfalls to Avoid

Even with the right intentions, poor execution can undermine Open Banking efforts. Here are five common pitfalls to avoid:

❌ Weak Governance: Without strong regulatory oversight and consistent enforcement, Open Banking risks becoming fragmented, limiting trust and scalability.

❌ Inadequate Stakeholder Engagement: Excluding key players—banks, fintechs, regulators, and consumer voices—erodes trust and slows adoption. Early, open dialogue builds consensus.

❌ Poor API Standardization: True standardization goes beyond agreeing on endpoints. It requires clear expectations across all aspects of API implementation: functional scope, performance benchmarks, security requirements, compliance KPIs, and support SLAs. Without this depth, interoperability remains superficial and expensive to sustain.

❌ Insufficient Consumer Protection: Cybersecurity lapses and unclear data policies undermine public trust. Without robust protection and transparency, adoption will falter.

❌ Ignoring Performance Metrics: Without well-defined KPIs and consistent monitoring, it's difficult to measure progress, drive improvements, or ensure accountability.

Conclusion: The Time for Action Is Now

Open Banking offers Africa a once-in-a-generation opportunity to rewire its financial systems for speed, inclusivity, and innovation. But this opportunity must be met with clarity and courage.

Now is the time for bold action: forward-looking regulation, fair competition, and strong public-private collaboration. With the right frameworks, Africa can do more than catch up. It can lead.

The question is no longer if Africa should adopt Open Banking, but how boldly and how fast.